Non-GAAP disclosure remains one of the most scrutinized areas of SEC reporting. Public companies use non-GAAP measures and other non-GAAP financial measures to explain operating performance and supplement GAAP results, but these disclosures remain a recurring source of SEC comment letters and enforcement actions when adjustments become misleading, inconsistent, or overly prominent.

Non-GAAP measures are governed primarily by Regulation G for public disclosures and Item 10(e) of Regulation S-K for SEC filings. The SEC non-GAAP disclosure rules focus on labeling, reconciliation, prominence, and the substance of adjustments themselves. This guide walks through the rules, recurring SEC comment patterns, reconciliation mechanics, presentation risks, enforcement examples, and practical review steps disclosure teams can use before filing.

What Counts as a Non-GAAP Measure

Under Regulation G, a non-GAAP financial measure is a numerical measure of historical or future financial performance, financial position, or cash flows that excludes amounts included in the most directly comparable GAAP measure, or includes amounts excluded from the comparable GAAP measure.

Common non-GAAP measures include:

- Adjusted EBITDA

- Adjusted net income

- Adjusted EPS

- Free cash flow

- Organic revenue growth

- Constant currency revenue

The definition applies to both historical and forward-looking disclosures, including adjusted guidance presented in earnings releases or SEC filings.

A core requirement in non-GAAP disclosure is identifying the "most directly comparable" GAAP measure. For example:

- Adjusted EBITDA is generally reconciled to net income.

- Free cash flow is typically reconciled to net cash provided by operating activities.

Not every operational metric or segment disclosure qualifies as a non-GAAP financial measure. Important exclusions include:

- Segment information presented in conformity with ASC 280 within the required segment-reporting framework

- Product revenue calculated directly in accordance with GAAP

However, total segment profit or loss presented outside the ASC 280 footnote reconciliation may become a non-GAAP measure subject to Regulation G and Item 10(e) of Regulation S-K.

For SEC reporting teams, classification is the first review step. Before evaluating reconciliation, labeling, or prominence, the company should determine whether the metric qualifies as a non-GAAP financial measure under the SEC's rules.

The Two Rule Sets: Regulation G and Item 10(e)

Regulation G Requirements

Regulation G applies to all public disclosures of non-GAAP measures by reporting companies. That includes earnings releases, investor presentations, earnings calls, conference presentations, and information posted on corporate websites.

The rule requires:

- Presentation of the most directly comparable GAAP measure

- A quantitative reconciliation between the GAAP and non-GAAP figures

The reconciliation should clearly identify each adjustment so investors can understand how the non-GAAP measure was calculated.

Rule 100(b) of Regulation G also prohibits non-GAAP measures that are materially misleading. The SEC may still challenge a measure even if a reconciliation is provided when the presentation obscures recurring expenses or distorts operating performance.

Because Regulation G applies beyond SEC filings, non-GAAP compliance controls should extend to investor relations materials, earnings-call scripts, executive presentations, and webcast preparation.

Item 10(e) Requirements for SEC Filings

Item 10(e) of Regulation S-K applies specifically to SEC filings and furnished earnings releases under Instruction 2 to Item 2.02 of Form 8-K.

In addition to the Regulation G reconciliation requirements, Item 10(e) requires:

- Equal or greater prominence for the comparable GAAP measure

- A quantitative reconciliation to the most directly comparable GAAP measure

- A statement explaining why management believes the non-GAAP measure is useful to investors

- Disclosure of any additional material purposes for which management uses the measure internally

For forward-looking non-GAAP measures, Item 10(e)(1)(i)(B) permits limited reconciliation exceptions where information is unavailable without unreasonable effort. Companies must still identify the unavailable information and explain its probable significance.

Prohibited Practices Under Item 10(e)

The SEC has identified several prohibited or high-risk non-GAAP disclosure practices:

- Excluding cash-settled charges or liabilities from non-GAAP liquidity measures other than EBIT or EBITDA

- Labeling charges as "non-recurring," "infrequent," or "unusual" when similar charges occurred within the prior two years or are reasonably likely to recur within two years

- Using titles that are confusingly similar to GAAP line items when the calculation differs materially from GAAP

- Presenting non-GAAP measures on the face of GAAP financial statements, in accompanying notes, or in Article 11 pro forma financial statements under Regulation S-X

These presentation issues are a recurring source of SEC comment letters and non-GAAP disclosure reviews. For SEC reporting teams, the operational focus is not only calculation accuracy, but also presentation balance, labeling discipline, and consistency across filings and earnings materials.

Recurring SEC Comment Themes

Recurring SEC comment-letter themes are heavily concentrated around adjustments, consistency, labeling, and presentation balance. Many of these issues appear repeatedly in Corp Fin Compliance & Disclosure Interpretations (C&DIs) and enforcement-related reviews.

Common SEC non-GAAP disclosure themes include:

- Excluding normal recurring operating expenses (C&DI 100.01) — The SEC has repeatedly challenged adjustments that remove ordinary cash operating expenses necessary to run the business. Comment letters often focus on expenses presented as "one-time" despite recurring operational patterns.

- Inconsistent adjustments between periods (C&DI 100.02) — Companies should not apply adjustments inconsistently across reporting periods without disclosure, recasting, or explanation.

- Excluding charges but retaining gains (C&DI 100.03) — The SEC frequently challenges asymmetrical treatment where companies remove losses or expenses while retaining related gains in the same reporting period.

- Individually tailored accounting principles (C&DI 100.04) — The SEC has stated that non-GAAP measures should not alter GAAP recognition or measurement principles. Examples include changing revenue-recognition timing or presenting revenue on a cash basis instead of accrual accounting.

- Improper labeling (C&DI 100.05) — Measures should clearly identify themselves as non-GAAP. Companies should also avoid using GAAP-style labels for differently calculated metrics.

- Improper "pro forma" terminology — The SEC generally expects "pro forma" labeling to remain limited to disclosures governed by Article 11 of Regulation S-X.

- Materially misleading measures (C&DI 100.06) — The SEC staff has stated that extensive disclosure cannot cure a materially misleading non-GAAP measure.

These issues represent some of the highest-frequency SEC comment-letter territory in non-GAAP compliance reviews. For issuer-side teams, the operational challenge is usually substantive review rather than reconciliation formatting alone. That is also where precedent-based review against actual SEC staff positions can materially improve consistency and disclosure discipline.

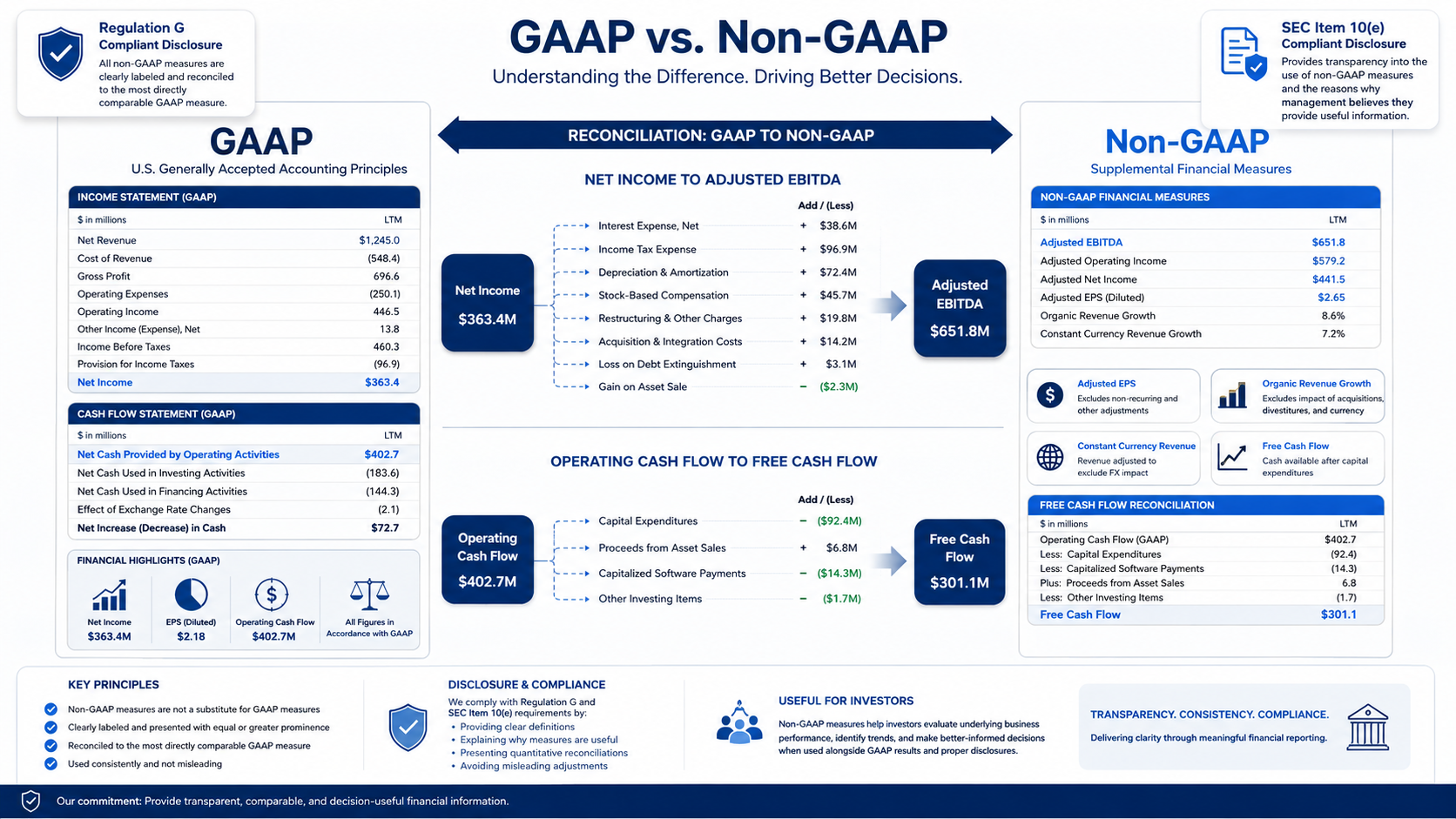

Reconciliation Requirements: What "Good" Looks Like

The SEC expects non-GAAP reconciliations to be detailed, internally consistent, and tied directly to the most directly comparable GAAP measure.

Strong non-GAAP disclosure practices generally include:

- Start the reconciliation with the comparable GAAP measure, not the non-GAAP figure.

- Identify each reconciling item separately with enough detail for investors to understand the nature of the adjustment.

- Present income tax effects as a separate, clearly explained adjustment rather than broadly describing measures as "net of tax."

- Reconcile EBITDA and EBITDA-based measures to net income rather than operating income.

- Label modified EBITDA measures as "Adjusted EBITDA" when additional company-specific exclusions are included.

- Present the three major categories of the statement of cash flows when discussing non-GAAP liquidity measures.

- Do not present liquidity measures on a per-share basis, including free cash flow per share.

- For forward-looking non-GAAP measures relying on the Item 10(e)(1)(i)(B) exception, disclose that the reconciliation is unavailable without unreasonable effort, identify the unavailable information, and explain its probable significance with equal or greater prominence.

Segment-based non-GAAP reconciliations remain a known SEC focus area. Where companies present operational metrics or segment profitability adjustments outside the ASC 280 framework, the methodology should remain consistent, documented, and defensible against challenge.

For SEC reporting teams, reconciliation quality is often the first indicator regulators use to assess the credibility of the broader disclosure process. Precedent-based workflows with traceable sources can help teams compare draft disclosures against prior filings, historical adjustments, and prior SEC comments before publication.

Prominence: Where Issuers Get Caught

Prominence issues remain one of the most common SEC non-GAAP disclosure review areas under C&DI 102.10. In many cases, the SEC challenge is not the adjustment itself, but how the measure is presented relative to the comparable GAAP metric.

Common undue-prominence issues include:

- Earnings-release headlines or captions that lead with non-GAAP measures while minimizing or delaying the comparable GAAP result

- Non-GAAP income statements composed primarily of non-GAAP line items mirroring a GAAP income statement, which the SEC staff views as inherently undue prominence

- Ratios using a non-GAAP numerator or denominator without presenting the comparable GAAP ratio

- Styling cues such as bold text, larger fonts, color emphasis, or placement that visually prioritize non-GAAP measures

- Descriptors such as "record performance" or "exceptional" applied only to the non-GAAP measure without equal treatment of the comparable GAAP metric

- Charts, graphs, or tables presenting non-GAAP measures without comparable GAAP visuals at equal or greater prominence

- Discussion and analysis focused heavily on the non-GAAP measure without similar discussion of the comparable GAAP result

For SEC reporting teams, prominence problems are often operational rather than accounting-driven. Many issues emerge during earnings-release drafting, investor-relations review, presentation design, or executive editing rather than during reconciliation preparation.

In practice, equal-or-greater prominence applies to more than formatting alone. The SEC also evaluates sequencing, narrative emphasis, visual structure, and whether the overall presentation could mislead investors about the company's actual GAAP performance.

Real Examples: Recent SEC Comments and Enforcement

Recent SEC comment letters and enforcement actions show recurring non-GAAP compliance patterns rather than isolated disclosure mistakes.

Representative non-GAAP disclosure examples include:

- MSG — The SEC questioned the company's adjustment for non-cash arena license fees added back to adjusted operating income, viewing the presentation as potentially individually tailored under C&DI 100.04. The company revised future disclosures.

- Commercial Metals — The SEC challenged the exclusion of mill operational commissioning costs from core EBITDA, viewing the costs as routine operating expenses rather than unusual adjustments. The company removed the adjustment going forward.

- RingCentral — The SEC cited Item 10(e) concerns after the company excluded cash interest and restructuring payments from unlevered free cash flow. The company later removed the adjustment from the metric.

- Lamb Weston and Accenture — Both companies received SEC comments related to labeling and segment-reconciliation practices. Each revised disclosures to improve labeling clarity and provide more detailed line-item reconciliations.

Some matters escalated beyond comment letters into enforcement actions:

- DXC Technology — In March 2023, the SEC charged the company over non-GAAP transaction-related adjustments that improperly classified ordinary operating expenses, overstating non-GAAP net income across multiple quarters. The matter resulted in an $8 million civil penalty.

- Newell Brands — In September 2023, the SEC charged the company and its former CEO over misleading non-GAAP core sales growth disclosures involving accelerated sales practices. The company agreed to pay a $12.5 million civil penalty, and the former CEO agreed to pay $110,000.

Across these matters, the SEC consistently focused on adjustment discipline, reconciliation support, labeling accuracy, review controls, and whether management's presentation could mislead investors about operating performance. These patterns also illustrate why stronger disclosure controls and precedent-based review workflows remain central to non-GAAP compliance.

Earnings Releases, Form 8-K, and the Item 2.02 Rules

Non-GAAP measures included in earnings releases furnished under Item 2.02 of Form 8-K remain subject to Item 10(e) of Regulation S-K. Companies must provide reconciliations, present the comparable GAAP measure with equal or greater prominence, and comply with the SEC's broader anti-misleading standards under Regulation G.

Instruction 2 to Item 2.02 also applies to oral presentations and earnings calls. If management discloses previously undisclosed material information during a webcast, conference call, or Q&A session, the company generally must make that information available on its website together with any required reconciliation materials.

Forward-looking non-GAAP financial measures such as adjusted guidance remain a recurring SEC review area. Even when companies rely on the Item 10(e)(1)(i)(B) unreasonable-effort exception, Regulation G still applies to the disclosure itself and to the overall presentation of the measure.

For SEC reporting teams, earnings releases remain a high-risk operational workflow because drafting, investor relations review, executive review, and legal signoff often occur on compressed timelines. Standardized reconciliation procedures and structured review controls can materially reduce non-GAAP compliance risk before publication.

Foreign Private Issuers and Special Cases

Regulation G provides a limited exception for certain foreign private issuer (FPI) non-GAAP disclosure. The exception generally applies when:

- The FPI's securities trade on a foreign exchange

- The non-GAAP financial measure is not derived from a U.S. GAAP measure

- The disclosure is released outside the United States only

Even where the Regulation G exception applies, Item 10(e) of Regulation S-K still governs non-GAAP financial measures included in Form 20-F filings and registration statements.

An FPI may also disclose an otherwise prohibited non-GAAP measure in an SEC filing when the measure is required by home-country law and included in the issuer's home-country annual report.

Section 101 of the SEC's non-GAAP C&DIs identifies additional special-case exclusions. Forecasts shared with a financial advisor during a business combination, and forecasts exchanged between transaction parties where disclosure is required under anti-fraud principles, are generally not treated as non-GAAP measures.

For multinational issuers, the operational challenge is usually maintaining consistency across home-country reporting rules, transaction disclosures, and SEC non-GAAP disclosure requirements.

Disclosure Controls: Building a Defensible Review Process

Exchange Act Rule 13a-15(a) requires issuers to maintain disclosure controls and procedures designed to ensure information is recorded, processed, summarized, and reported appropriately. Applied to non-GAAP compliance, that means companies should maintain formal review controls around how non-GAAP measures are defined, adjusted, reconciled, approved, and presented.

A defensible non-GAAP disclosure process typically includes:

- A written non-GAAP policy with defined measures, defined adjustment categories, named process owners, and documented change-control procedures

- Period-over-period consistency testing for each adjustment

- Source-document support tied to every adjustment with identified approvers

- Reconciliations built directly into the disclosure workflow rather than added as a downstream exercise

- Prominence testing across headlines, captions, body text, ratios, charts, and tables

- Tracking every SEC comment-letter response and incorporating the resolution into the company's disclosure policy

Many non-GAAP disclosure failures originate from workflow breakdowns rather than accounting mechanics alone. When reconciliation review, prominence testing, and consistency analysis occur too late in the drafting cycle, companies increase the risk of unsupported adjustments, inconsistent presentation, and SEC review comments.

This is also where precedent-based workflows with traceable sources can strengthen disclosure controls. Dimension AI supports review workflows that compare draft disclosures against the universe of public filings, surface inconsistencies, and produce audit trails for every change without generating text. Outputs are auditable and verifiable, every output can be audited back to its source, and we never train external AI models on your data.

For SEC reporting teams and disclosure committees, the operational goal is building the review layer that closes the gap between policy and filing.

Pre-Filing Non-GAAP Review Checklist

Before publication, disclosure teams should complete a structured non-GAAP compliance review across definitions, reconciliation, prominence, adjustment consistency, and documentation controls.

Definitions and labels

- Confirm each non-GAAP financial measure is clearly identified as non-GAAP

- Verify labels do not resemble GAAP line items

- Confirm consistent terminology across filings, releases, and presentations

Reconciliation

- Reconcile each measure to the most directly comparable GAAP measure

- Start each reconciliation with the GAAP figure

- Confirm line-item support for every adjustment

Prominence

- Test headlines, captions, charts, tables, ratios, and body text for equal-or-greater GAAP prominence

- Confirm liquidity measures are not presented on a per-share basis

Adjustments and consistency

- Test each adjustment for period-over-period consistency

- Compare current-period adjustments against prior filings and SEC comments

- Evaluate whether new adjustments require revised disclosure language

Controls and documentation

- Tie every adjustment to source documentation

- Confirm named approvers and review sign-offs

- Maintain records of SEC comment-letter responses and related policy updates

This checklist is intended as a structural review tool, not a substitute for counsel review or auditor sign-off on novel or material adjustments.

Frequently Asked Questions

What is the difference between Regulation G and Item 10(e)?

Regulation G applies broadly to public disclosures containing non-GAAP measures, including earnings releases, investor presentations, and earnings calls. It requires presentation of the most directly comparable GAAP measure together with a quantitative reconciliation.

Item 10(e) of Regulation S-K applies specifically to SEC filings and earnings releases furnished under Item 2.02 of Form 8-K. It adds requirements around equal-or-greater prominence, management-usefulness disclosure, and prohibited presentation practices.

What is the most common SEC criticism of non-GAAP disclosures?

One of the most common SEC criticisms involves excluding normal, recurring cash operating expenses from non-GAAP financial measures. The SEC addresses this directly in C&DI 100.01.

The SEC also frequently challenges prominence issues under C&DI 102.10, including headlines, charts, tables, and narrative discussion that emphasize non-GAAP results more heavily than comparable GAAP measures.

How should EBITDA and Adjusted EBITDA be reconciled?

EBITDA is generally reconciled to net income rather than operating income. If a company adds additional adjustments beyond standard EBITDA components, the measure should generally be labeled "Adjusted EBITDA."

The reconciliation should begin with the comparable GAAP figure and identify each adjustment separately.

Can a non-GAAP measure be presented on a per-share basis?

Non-GAAP liquidity measures cannot be presented on a per-share basis under Item 10(e). That prohibition includes free cash flow per share.

Performance measures such as adjusted EPS are generally permitted if they comply with reconciliation and prominence requirements.

What does "equal or greater prominence" mean in practice?

The comparable GAAP measure cannot be visually or contextually minimized relative to the non-GAAP figure.

The SEC has challenged disclosures using larger fonts, bold styling, headline placement, charts, or narrative emphasis that prioritize non-GAAP performance while minimizing GAAP results.

Are non-GAAP measures in earnings releases subject to the same rules as SEC filings?

Yes. Earnings releases furnished under Item 2.02 of Form 8-K remain subject to Item 10(e) reconciliation and prominence requirements, in addition to Regulation G.

Closing Thoughts

Non-GAAP disclosure remains one of the highest-frequency SEC review areas because small presentation, reconciliation, or consistency issues can materially change how investors interpret performance. Regulation G, Item 10(e), the SEC's C&DIs, and recent enforcement actions all point toward the same operational conclusion: companies need disciplined review controls, consistent adjustment policies, and defensible disclosure workflows.

For disclosure committees, legal teams, investor relations, and SEC reporting groups, non-GAAP compliance is not only about preparing reconciliations correctly. It is also about maintaining auditability, consistency, and governance across every stage of the drafting and review process.

See how a precedent-based review layer compares your draft disclosures against the universe of public filings — with traceable sources and full audit trails. Request access.

To access this endpoint, you must have an approved developer account, and have activated the new developer portal. When authenticating, you must use keys and tokens from a developer App that is located within a Project. Learn more about getting access to the API v2 endpoints in our "Getting started" page:

Once you have the API v2 collection loaded in Postman

The hide replies endpoint uses OAuth 1.0a user context authentication. If successful, the endpoint hides a single Reply that was published in a Tweet conversation that was initiated by an authenticated user. Each conversation supports hiding up to 725

This endpoint gives you the ability to programmatically hide or unhide replies using criteria you define. Just like the functionality in the main

There are several different tools and libraries that you can use to make a request to this endpoint, but we are going to use the Postman tool here to simplify the process.